Why Hype Carries Both Fraud and Signal

The dangerous thing about hype is not that it is false, it is that it is partly true.

In 1879 a man named John Worrell Keely demonstrated a motor in Philadelphia that ran, he claimed, on energy extracted from the vibration of water. Investors gave him the equivalent of millions in today's money. The demonstrations were genuinely impressive. Machines moved. Witnesses signed statements. The Keely Motor Company traded on the strength of these demos for nearly two decades. When Keely died in 1898 and investigators finally opened the floor beneath his laboratory, they found a hidden compressed-air system feeding the machines through the floorboards.

The reason I open with a fraud rather than a triumph is that pure fraud is the easy case. Keely had nothing. Once you found the air hose, the question was closed. The hard cases, the cases that actually cost serious people serious money and time, are the ones where the demo is not faked at all. The machine really does move. The capability is real. It just does not generalize, or it does not survive contact with production, or it costs ten times what the demo implied. Hype is dangerous precisely because it is rarely Keely. It is usually a true thing wearing the costume of a much larger true thing.

This chapter is about learning to see both at once: the fraud and the signal, riding the same wave, and refusing to throw out the second when you spot the first.

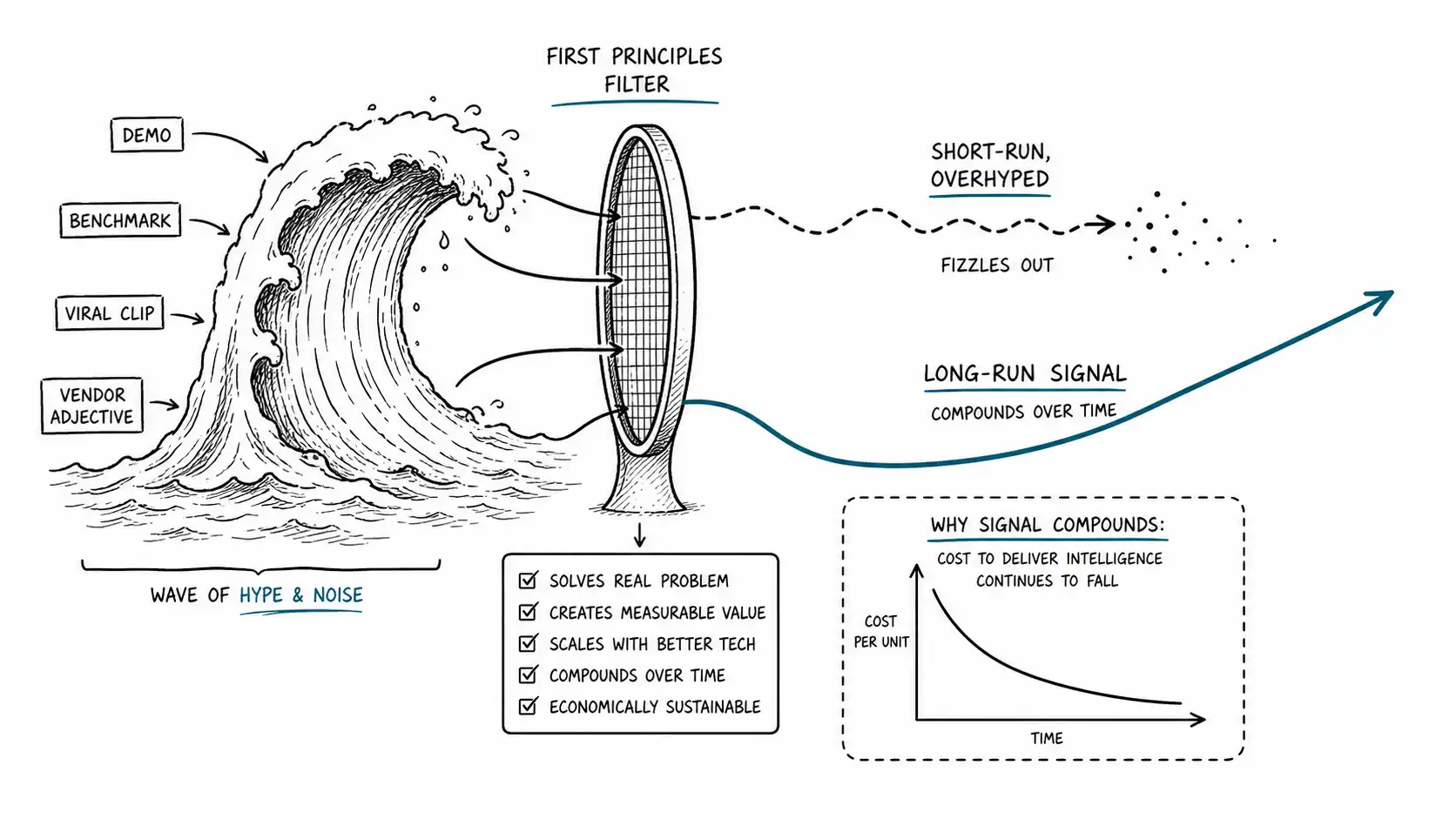

The shape of the wave

The most famous map of this terrain is Gartner's Hype Cycle, which tracks a technology through five named stages: the innovation trigger, the peak of inflated expectations, the trough of disillusionment, the slope of enlightenment, and the plateau of productivity. In Gartner's 2024 and 2025 framings, generative AI is described as having crossed the peak and entered the trough, while agentic AI rides up toward its own peak (Gartner, Hype Cycle for Emerging Technologies).

I find the Hype Cycle useful as a vocabulary and untrustworthy as a measurement, and it is worth being honest about why. The curve has no axes you can actually quantify. "Expectations" is not measured in any unit. The position of a technology on the curve is assigned by analyst judgment, not derived from data, which means the curve can never be falsified: whatever happens, the technology was simply at the stage that explains it. A model that always fits is a model that never predicts. Independent reviews of Gartner's own placements over multiple years show technologies appearing, disappearing, and being renamed in ways that do not trace a clean curve at all (Pragmatic Coders analysis of four years of Gartner AI placements).

So use the Hype Cycle the way you would use the words "spring" and "winter": as seasons, not as a thermometer. It tells you that excitement and disappointment tend to come in that order. It does not tell you where on the curve your specific decision sits, and it certainly does not tell you whether a given technology will reach the plateau at all. Plenty never do. The curve quietly drops them.

Amara's Law and the two errors

The more durable idea, and the one I reach for constantly, comes from Roy Amara, who ran the Institute for the Future and around 1978 articulated what became known as Amara's Law: we tend to overestimate the effect of a technology in the short run and underestimate the effect in the long run (Roy Amara, via Institute for the Future history).

Notice what Amara's Law actually claims, because it is more useful than the cliche it has become. It does not say technology is overhyped. It says the same technology is simultaneously overhyped on a short horizon and underhyped on a long one. The error is not in the direction of belief. The error is in the matching of the belief to the timescale.

This is the engine of the whole problem. When the agent demo went viral, the founder who said "we are behind" was making the short-run error: assuming the capability shown would be in production everywhere within the quarter. The cynic on the same team who said "agents are a toy" was making the long-run error: assuming that because it was not production-ready now, it never would be. Both were wrong, and they were wrong by exactly the amount that Amara warned about. The signal and the fraud were the same event seen on two different clocks.

Amara, by the way, defined "short" as roughly ten years and "long" as roughly twenty. Internet time has compressed those numbers, but the structure holds. The practical move is never to ask "is this overhyped or underhyped." It is to ask "on what timescale, and for whom, is this claim true."

Why the wave carries fraud

If the technology is partly real, why is the wave so thick with deception? Because the structure of an early market rewards it. I have built the deception side, so let me describe the mechanics without flinching.

A demo is a controlled environment optimized for a single successful run. When I produced launch videos, the rule was never to fake the result, that is Keely, that is illegal and stupid, but to choose the one input out of fifty where the result was clean and to film that one. The forty-nine failures were not lies. They simply were not in frame. The viewer sees a fifty for fifty system. The system is closer to one for fifty, and the difference between those two numbers is the entire gap between a demo and a deployment.

Add to this the incentives of the surrounding ecosystem. The lab that shipped the model wants adoption, so it leads with the best case. The analysts who cover the lab need access, so they soften the qualifications. The influencers who post the clip are rewarded by an algorithm that pays for amazement, not for accuracy, so the most breathless framing travels furthest. The competitors feel the pressure and ship their own clips. None of this requires anyone to be a fraud. It requires only that everyone in the chain be slightly, rationally, optimistic in their own interest. The sum of many small optimisms is a claim much larger than the underlying truth. That is the fraud component, and it is structural, not personal.

Why the wave carries signal

And yet. Underneath the inflated claim there is almost always a real capability that did not exist before, and dismissing the whole wave because the top of it is inflated is how you miss the thing that actually changes your business.

The signal is real because the underlying numbers move in ways that are not hype at all. Consider inference cost. According to the Stanford AI Index, the cost to run a model at GPT-3.5 level fell more than 280-fold between late 2022 and late 2024, from roughly twenty dollars per million tokens to about seven cents (Stanford HAI, 2025 AI Index Report). That is not a claim on a leaderboard or a clip on a feed. That is a cost curve, and a cost curve that bends by two orders of magnitude in two years changes which use cases are economically viable, whatever the influencers say. A workflow that was absurd at twenty dollars per million tokens is routine at seven cents.

This is the signal that Amara's long run is made of. The short-run noise is the demo of the agent booking your flights. The long-run signal is the cost of intelligence falling far enough that uses nobody filmed become quietly, boringly profitable. The skill is to ignore the first while tracking the second, and they arrive in the same announcement.

Separating them in practice

You cannot eliminate the fraud component or guarantee the signal. What you can do is run incoming claims through a separator before they reach your roadmap. Here is the one I use, and I will formalize the first stage into a named filter in the next chapter.

The first move is to restate the claim in your own words, stripped of the vendor's adjectives. "Autonomous agent that handles your operations" becomes "a model that, given a goal and tool access, can chain several tool calls and sometimes complete a multi-step task without human intervention." The restatement is not cynicism. It is translation, and the act of translating usually drains half the inflation by itself, because adjectives do not survive being rephrased.

The second move is to ask the timescale question explicitly, in Amara's terms. Split the claim into a short-run version and a long-run version and evaluate them separately. The short-run version of the agent claim, "we can hand our operations to this today," is almost certainly false. The long-run version, "models will increasingly complete multi-step tasks with declining supervision, and the cost of trying will keep falling," is almost certainly true. Once you have both, you stop arguing about whether the claim is real, because you have agreed it is both, and you start arguing about the only thing that matters: which version governs the decision in front of you.

The third move is to locate the hidden assumption. Every inflated claim rests on one assumption that, if false, collapses the whole thing for your situation. For the agent demo it was usually reliability: the demo assumed a success rate that, multiplied across the five or six steps of a real workflow, produced an end-to-end success rate too low to ship. Five steps at ninety percent each is under sixty percent end to end. Finding that assumption is finding the seam between the signal and the fraud.

The table below is how I log the separation for a claim, so that the same claim cannot come back next month and re-litigate itself.

| Element | What I write down |

|---|---|

| Raw claim (their words) | The headline, verbatim, adjectives included |

| Restated claim (my words) | Same capability, no marketing language |

| Short-run version | What is being implied is true today |

| Long-run version | What is plausibly true over a few years |

| Load-bearing assumption | The one thing that, if false, makes it irrelevant to us |

| Signal worth tracking | The underlying trend, if any, independent of this product |

| Decision it should touch | Specifically which of our decisions, or none |

A note on Christensen, used carefully

It is tempting at this point to invoke Clayton Christensen and "disruptive innovation," because every hyped technology is sold as the disruption that ends your business. I want to use the idea carefully, because it is widely misused. Christensen's actual claim was narrow: that certain innovations enter at the low end or in new markets, underperform on the metrics incumbents care about, and improve until they are good enough to take the mainstream (Christensen, The Innovator's Dilemma, summarized in Diffusion of Innovations literature). It was never a theory that everything new disrupts everything old. Most new technology sustains existing players rather than disrupting them.

The careful use, for our purposes, is this. When a claim arrives, ask whether it looks like a sustaining improvement to something you already do, in which case your incumbent advantages apply and you have time, or whether it looks like a genuinely cheaper, worse-on-your-metrics entrant that is improving fast, in which case the cost curve, not the demo, is the thing to watch. The cost curve is where the disruption hides, which is why I trust the inference-cost number more than any leaderboard.

Summary

Hype is not a lie to be dismissed or a prophecy to be obeyed. It is a true capability inflated by a chain of rational optimisms, riding the same wave as a real long-run trend. The Hype Cycle gives you seasons but not measurements. Amara's Law tells you the error is in the timescale, not the direction. The job is to separate the short-run fraud from the long-run signal before either reaches your roadmap, and to log that separation so the claim cannot re-run the meeting next quarter.

Key Takeaways

- The expensive cases are not fakes like Keely's motor. They are real capabilities that do not generalize, do not survive production, or cost far more than the demo implied.

- Treat Gartner's Hype Cycle as seasonal vocabulary, not measurement. It has no quantified axes and cannot be falsified, so it predicts nothing about your specific decision.

- Amara's Law says the same technology is overhyped short term and underhyped long term. The error is in matching belief to timescale, not in the direction of belief.

- The fraud component is structural: a chain of rational optimisms, from lab to analyst to influencer to competitor, sums to a claim far larger than the truth, with no single liar required.

- The signal component is real and measurable: inference cost falling more than 280-fold in two years changes which use cases are viable regardless of the feed.

- Separate every claim into short-run and long-run versions, find the one load-bearing assumption, and log it so the claim cannot re-litigate itself next month.

- Use Christensen narrowly: watch the cost curve, not the demo, because that is where genuine disruption hides.